Tax documents organized on a home office desk

Tax Documents You Need to File Your Return

Content

Content

Gathering the right paperwork before tax season arrives saves hours of frustration and helps you claim every deduction you're entitled to. The IRS requires specific forms and records to verify your income, expenses, and eligibility for credits. Missing even one document can delay your refund by weeks or trigger an audit years later.

Most taxpayers need at least five to ten different forms, though self-employed workers and those with complex finances may need dozens. The exact mix depends on your income sources, life changes during the year, and which deductions you plan to claim. Starting your collection in January gives you time to request replacements if something doesn't arrive.

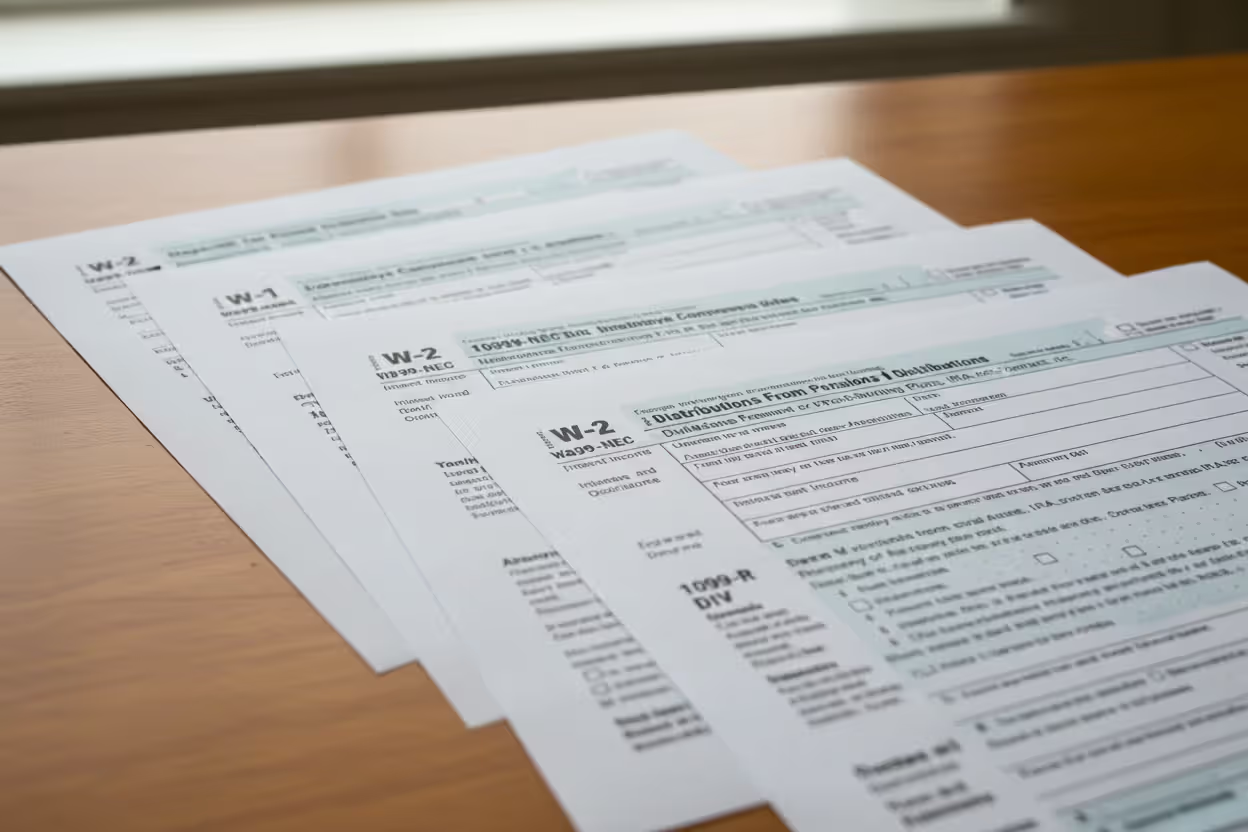

Income Records and Earning Statements

Every dollar you earn must be reported, and the IRS receives copies of most income statements sent to you. Employers issue Form W-2 by January 31st, showing wages, tips, and withheld taxes. Check that your name and Social Security number match your records exactly—mismatches trigger automatic processing delays.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Independent contractors and freelancers receive Form 1099-NEC for payments of $600 or more. Banks and brokerages send 1099-INT for interest income over $10 and 1099-DIV for dividends. Investment sales appear on Form 1099-B, which includes cost basis information your broker reported to the IRS. Cryptocurrency exchanges now send 1099-DA forms for digital asset transactions.

Partnership and S-corporation owners need Schedule K-1, which shows their share of business income, deductions, and credits. These forms often arrive late—sometimes not until mid-March—because the business must finalize its return first. If you sold stocks, rental property, or a business during the year, gather purchase records and improvement receipts to calculate your actual gain or loss.

Unemployment compensation appears on Form 1099-G from your state workforce agency. Social Security and railroad retirement benefits come on Form SSA-1099 or RRB-1099. Even if you had taxes withheld from these payments, you must report the full amount. Pension and IRA distributions require Form 1099-R, which codes whether the money was a normal distribution, early withdrawal, or rollover.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Deduction and Credit Documentation

Standard deduction amounts increased significantly in recent years, meaning fewer taxpayers benefit from itemizing. For 2025 returns filed in 2026, the standard deduction is $15,000 for single filers and $30,000 for married couples. You only itemize if your combined deductions exceed these thresholds.

Mortgage lenders send Form 1098 showing home loan interest paid. Property tax bills from your county treasurer verify real estate taxes, though these amounts also appear in your mortgage statement if you pay through escrow. Home equity loan interest is only deductible if you used the money to substantially improve the home securing the loan.

Charitable donations require written acknowledgment from the organization for any single gift of $250 or more. The receipt must state whether you received anything in return. Donating a car, boat, or property worth over $500 requires additional forms. Non-cash donations under $250 need a detailed list with acquisition dates and fair market values—a Goodwill drop-off receipt alone won't suffice if you're audited.

Education expenses qualify for credits if you have Form 1098-T from your school. The American Opportunity Tax Credit offers up to $2,500 per student for the first four years of undergraduate study. The Lifetime Learning Credit covers graduate school and professional development courses. Keep receipts for required textbooks and supplies, which count toward the American Opportunity Credit but not Lifetime Learning.

Medical expenses must exceed 7.5% of your adjusted gross income to provide any benefit. Save receipts for insurance premiums not paid through pre-tax payroll deductions, prescription costs, dental work, and mileage to medical appointments at 21 cents per mile for 2025. Long-term care insurance premiums have age-based deduction limits.

Business expenses for employees are no longer deductible under current law, but teachers can still claim up to $300 for classroom supplies. Self-employed individuals deduct ordinary and necessary business costs on Schedule C, requiring detailed records covered in a later section.

Receipts Worth Keeping

Not every receipt matters. Grocery store purchases don't qualify unless you're tracking a specific medical diet prescribed by a doctor. Restaurant meals are only 50% deductible for self-employed individuals entertaining clients, and you must note the business purpose and attendees on the receipt.

Focus on big-ticket items: medical procedures, property tax payments, major charitable gifts, and business equipment. Monthly credit card statements work as backup documentation if they show the vendor name and amount, though you'll need the original receipt to prove business purpose during an audit.

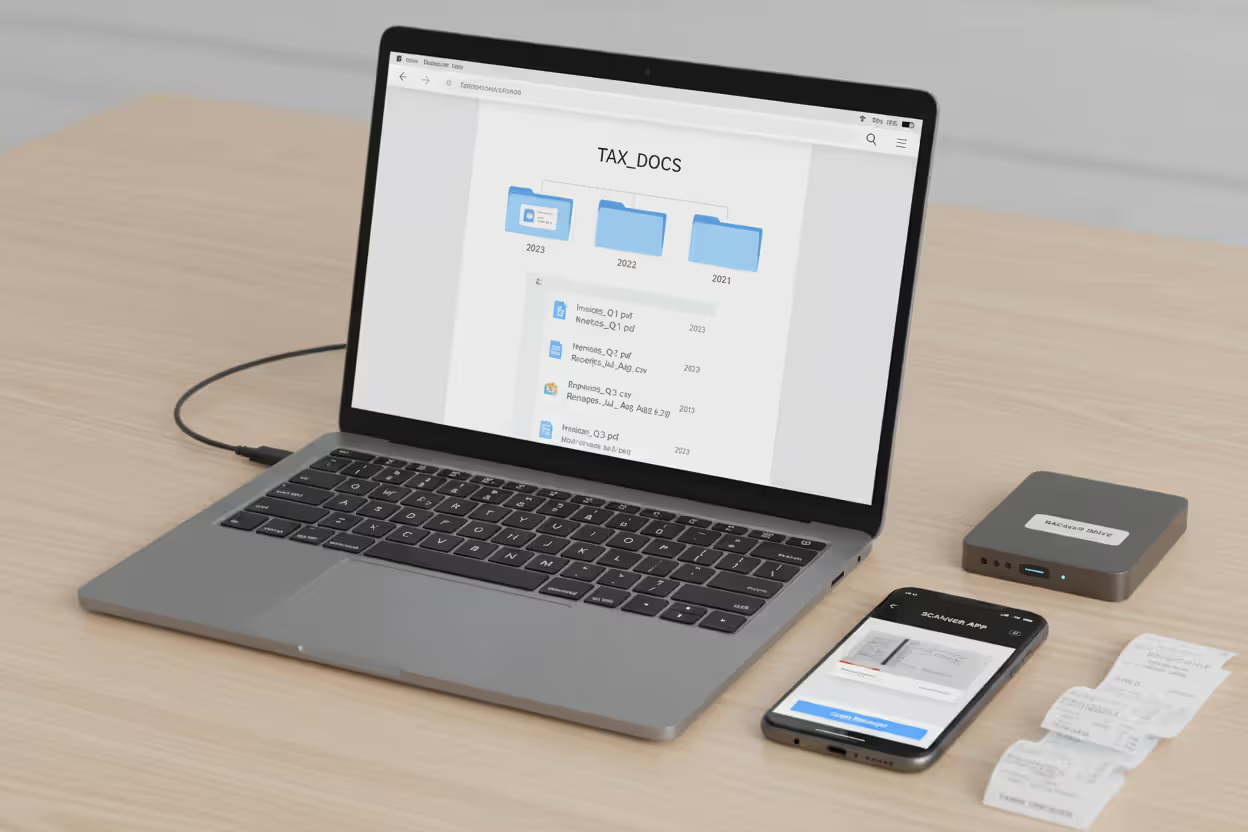

Digital vs. Paper Records

The IRS accepts scanned documents and photos of receipts as long as the images are clear and legible. Phone apps like Evernote or Expensify timestamp photos and sync to cloud storage. Many banks now offer document vaults that preserve statements for seven years.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Paper records fade, especially thermal-printed receipts from gas stations and retailers. Photocopy or scan these within a few months. Store originals in a fireproof safe or bank safety deposit box if they represent large transactions. Keep digital backups in at least two locations—a local hard drive and a cloud service.

Personal Identification and Prior Year Returns

Every person listed on your return needs a Social Security number or Individual Taxpayer Identification Number (ITIN). This includes you, your spouse, and all dependents. Children without Social Security numbers by the filing deadline can't be claimed, costing you thousands in credits.

Your driver's license or state ID verifies your identity if you're filing electronically for the first time or after a name change. The IRS matches your adjusted gross income from last year's return as an additional security check. Pull your 2024 return before you start—you'll need it to answer security questions and carry forward items like capital loss carryovers or unused education credits.

Bank account and routing numbers enable direct deposit of your refund, which arrives in 10-14 days versus six weeks for paper checks. Verify these numbers from a check or bank statement rather than typing from memory. One wrong digit sends your refund to someone else's account, requiring months to recover.

Documents for Self-Employed and Gig Workers

Side hustles and freelance income create the most complex tax situations. Form 1099-NEC arrives from each client who paid you $600 or more, but you must report all income even if you earned less from a particular source. Payment apps like Venmo and PayPal send Form 1099-K if your business transactions exceeded $5,000 in 2025—the threshold has been gradually lowering.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Business expense receipts reduce your taxable income dollar-for-dollar. Track office supplies, software subscriptions, professional development courses, business insurance, and advertising costs. Equipment purchases over $2,500 are typically depreciated over several years, though Section 179 expensing lets you deduct the full amount immediately up to $1,220,000 in 2025.

Mileage logs must include date, destination, business purpose, and miles driven for each trip. The standard rate of 70 cents per mile for 2025 covers gas, maintenance, insurance, and depreciation. Alternatively, track actual expenses and multiply by your business use percentage, though this requires more detailed records. Most drivers benefit from the standard rate unless they drive a luxury vehicle.

Home office deductions require exclusive and regular business use of a specific area. Measure your office space in square feet and divide by your home's total square footage. Multiply this percentage by mortgage interest, property taxes, utilities, and repairs. The simplified method allows $5 per square foot up to 300 square feet, requiring no receipts but offering a smaller deduction.

Estimated tax payment records prove you paid quarterly installments. Save the confirmation numbers from IRS Direct Pay or copies of mailed vouchers. Underpayment penalties apply if you didn't pay enough throughout the year, but you can request a waiver for reasonable cause.

Life Event Documentation

Major life changes trigger tax implications. Marriage certificates let you file jointly, usually reducing your combined tax bill. Divorce decrees specify which parent claims children as dependents and who deducts alimony under older agreements—alimony from divorces finalized after 2018 is neither deductible nor taxable.

Adoption papers and the adoption taxpayer identification number from your social services agency qualify you for the adoption credit, which covers up to $16,810 per child in 2025. Foster parents receive non-taxable reimbursements that don't need to be reported.

Health insurance forms prove you had qualifying coverage all year. Form 1095-A comes from marketplace plans and calculates premium tax credit reconciliation. Forms 1095-B and 1095-C from employers and insurers verify coverage but don't require any action for most people. A few states still impose individual mandate penalties, requiring proof of coverage.

Retirement account distributions need careful documentation. Form 1099-R codes whether you took a normal distribution, rolled money to another account, or withdrew early with a penalty exception. First-time homebuyers, college expenses, and certain medical costs allow penalty-free early withdrawals from IRAs if properly documented.

How to Organize Your Tax Paperwork

Create a dedicated folder or envelope each January labeled with the tax year. Drop every tax-related document inside as it arrives. This prevents the April scramble through junk drawers and email folders.

Set up a simple filing system: one section for income forms, another for deduction receipts, and a third for prior year returns. Subdivide further if you have rental properties or multiple businesses. Label everything clearly—"2025 Medical Receipts" beats a folder marked "Misc."

Digital scanning works best immediately upon receipt. Photograph receipts the day you get them, then file or discard the paper. Create a folder structure on your computer mirroring your physical files. Use consistent naming conventions like "2025-01-15_Medical_Dentist_$350.pdf" so files sort chronologically and remain searchable.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Most tax forms arrive by early February, but some stragglers appear until mid-March. Brokerage firms have until February 15th to send corrected 1099s if they discover errors. Partnership K-1s often arrive late. If you're missing a form by mid-February, contact the issuer directly—their phone number appears on last year's copy.

Request wage and income transcripts from the IRS if a form never arrives. These free reports show what the IRS received under your Social Security number. Allow 7-10 business days for mail delivery or access them immediately through the IRS website with identity verification.

How Long to Keep Tax Documents After Filing

The IRS has three years from your filing date to audit most returns, but this extends to six years if you underreported income by more than 25%. No statute of limitations exists if you never filed or committed fraud. Tax professionals recommend keeping returns and supporting documents for at least seven years.

Tax Document Retention Guide

| Document Type | Retention Period | Reason | Disposal Method |

| Filed tax returns | Permanent | Reference for future filings, loan applications, Social Security benefit calculations | Never discard |

| W-2s, 1099s, K-1s | 7 years | Verify income reporting, defend against audits | Shred after period expires |

| Receipts for deductions | 7 years | Prove claimed expenses during audit | Shred after period expires |

| Property purchase records | Until sale + 7 years | Calculate capital gains, prove cost basis | Shred 7 years after selling |

| Home improvement receipts | Until sale + 7 years | Increase cost basis, reduce taxable gain | Shred 7 years after selling |

| Retirement account records | Until distribution + 7 years | Track basis in after-tax contributions | Shred 7 years after final distribution |

Store documents in a fireproof safe or safety deposit box while in the retention period. Digital files should live on encrypted drives with cloud backup. When disposal time arrives, shred paper documents or use a professional document destruction service. Simply deleting digital files isn't enough—use secure deletion software that overwrites data multiple times.

Some records deserve permanent storage. Keep all filed returns forever—you'll need them for Social Security benefit calculations, pension applications, and proving prior tax payments if the IRS loses records. Investment purchase records must be kept until you sell the asset plus seven years to prove your cost basis.

The single biggest mistake I see is taxpayers waiting until April to gather their paperwork. Starting in January gives you time to track down missing forms, discover overlooked deductions, and make last-minute retirement contributions before the deadline. Clients who bring organized records save 30-40% on preparation fees and catch more deductions because we're not rushing through shoebox receipts

— Jennifer Martinez

Frequently Asked Questions

Tax preparation becomes manageable when you treat document gathering as a process rather than a crisis. Start collecting paperwork in January, verify everything arrives by mid-February, and reach out for replacements immediately if something's missing. Organized records reduce preparation time, lower professional fees, and provide peace of mind if the IRS ever questions your return.

The specific documents you need depend entirely on your financial situation, but everyone requires proof of income, identification, and prior year returns at minimum. Deductions and credits demand additional evidence—the more you claim, the more documentation you'll need. Self-employed individuals face the heaviest burden, tracking dozens of expense categories throughout the year.

Digital tools have simplified record-keeping, but they don't eliminate the need for systematic organization. Take photos of receipts immediately, maintain a dedicated folder for tax documents, and back up everything to multiple locations. When disposal time comes, shred thoroughly rather than tossing documents in the trash where identity thieves can access them.

The effort you invest in gathering and organizing your tax paperwork pays dividends beyond just filing your return. Complete records let you spot tax-saving opportunities, defend your positions during audits, and avoid penalties for missing information. Start building these habits now, and tax season will transform from a dreaded chore into a routine task you complete with confidence.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to tax filing, tax software, IRS forms, deadlines, and general tax preparation processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Tax filing requirements may vary depending on individual circumstances, income sources, residency status, and applicable laws.

This website does not provide tax, legal, or financial advice, and the information presented should not be used as a substitute for consultation with a qualified tax professional or advisor.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.