Person reviewing a simple tax return on a laptop with W-2 forms on a desk

Simple Tax Return Guide for US Taxpayers

Content

Content

Most Americans overthink their taxes. If you're drawing a regular paycheck and not running a side business, chances are your return takes less time than binge-watching two episodes of your favorite show. The trick? Knowing whether you actually need all those bells and whistles tax software companies try to sell you—or if you qualify for the genuinely free route.

What Is a Simple Tax Return?

Here's something the IRS won't tell you outright: they don't actually label returns "simple" or "complicated." That's marketing speak from tax prep companies. But the distinction matters because it determines whether you're spending $0 or $200+ on filing.

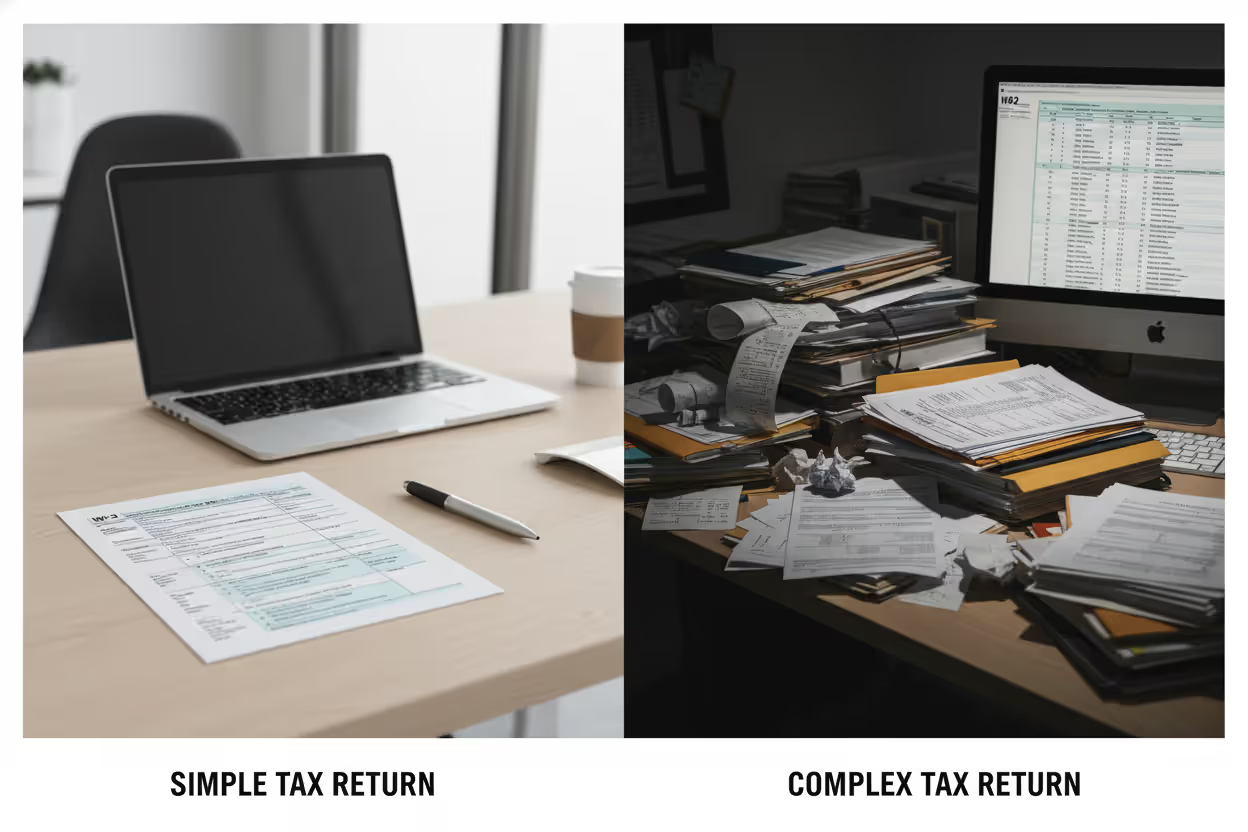

Think of a simple return this way—it's any filing that sticks to the basics. You're reporting money from a regular job (that's your W-2), taking the deduction everyone gets automatically (the standard deduction), and maybe claiming one or two common breaks like the credit for having kids. The whole thing fits on the main tax form without needing a bunch of extra paperwork stapled on.

Now contrast that with what tax pros deal with when someone walks in with rental properties, stock trades, a consulting business, and receipts stuffed in a shoebox. Those returns need Schedule C for business stuff, Schedule D for investment sales, Schedule E for rental income—sometimes a dozen different forms. It's not the number of pages that makes it complex, though. It's needing specialized knowledge to avoid screwing up.

A basic tax return typically means you've got W-2 income under six figures, you're not tracking business mileage or home office deductions, and your "investment portfolio" amounts to a savings account earning $47 in interest. The IRS data from recent years shows about 37% of individual filers fall into this category, though many don't realize it and pay for help they don't need.

Author: Benjamin Carte;

Source: atiservicesoftampa.com

Who Qualifies for a Simple Return?

Here's what actually determines if you're a simple filer—it's not about how much you earn. It's about where that money comes from.

The clearest candidates? You work a regular job (or maybe two), you get W-2s in January, you're not itemizing a bunch of deductions, and you don't own a business. That's it. You could make $85,000 at your job and still have a dead-simple return. Meanwhile, someone earning $30,000 who drives for Uber on weekends needs a complex filing because of that self-employment income.

For 2026, single folks under 65 must file when they hit $14,600 in income. Married couples filing together need to file at $29,200. Notice those numbers match the standard deduction amounts—meaning if you're required to file at all, you probably qualify for simple filing if you're only reporting employment wages.

You're definitely in simple territory if you:

- Get all your income from jobs (just W-2 forms, maybe from one or two employers)

- Take the standard deduction instead of itemizing ($14,600 if you're single, $29,200 married filing jointly, $21,900 as head of household for 2026)

- Only have unemployment payments beyond your regular wages

- Claim standard credits like the Child Tax Credit or Earned Income Tax Credit without exotic add-ons

- Earned under $1,500 in regular savings account interest

- Receive Social Security plus a straightforward pension and nothing else

You've crossed into complex territory when you're freelancing, renting out property, selling investments or crypto, dealing with foreign bank accounts, claiming education credits that need receipts, or itemizing medical bills and charity donations.

Your filing status—single, married, head of household—doesn't complicate things much by itself. Two married people with two W-2s and two kids? Still simple. One single person with freelance income and a home office deduction? Complex, regardless of the dollars involved.

Forms Used for Basic Tax Filing

The Form 1040 handles everything now. The IRS redesigned it a few years back to work for everyone, from the simplest filer to someone with a complicated financial life. For basic situations, you're really only dealing with the first two pages—wages go on line 1a (pulled from your W-2), you claim your standard deduction on line 12, and the form does the math to tell you if you owe money or get a refund.

Taxpayers 65 and up can use Form 1040-SR instead. Same information, just bigger print and a chart printed right on the form showing standard deduction amounts. You don't have to use it—plenty of seniors stick with the regular 1040. It's purely about readability.

Remember Form 1040-EZ? That disappeared after 2017. The current 1040 absorbed its job. Some people still hunt for it online, not realizing the "simplified" form they want is just the regular 1040 when you've got a straightforward situation.

States run their own show. Florida, Texas, and Washington residents skip state returns entirely—no income tax. California and New York require separate filings that might or might not mirror your federal simplicity. A handful of states offer one-page returns for W-2-only residents, while others make everyone use the same form regardless.

| Form Type | Who It's For | Key Features | Limitations |

| Form 1040 | Every individual taxpayer | Two-page main form; add schedules only when needed; handles simple to complex situations | None—it's the universal form everyone uses |

| Form 1040-SR | Anyone 65 or older | Larger type for easier reading; standard deduction chart built in; content identical to regular 1040 | Must be 65+; no real advantage except readability |

| Schedule 1 | Anyone with extra income or adjustments | Where unemployment income goes; student loan interest deduction; HSA contributions | Even simple filers need this for certain common items |

| Schedule 2 | People owing extra taxes | Alternative minimum tax; repaying too much health insurance subsidy | Simple filers rarely touch this |

| Schedule 3 | Claiming specific credits | Education credits; foreign tax credit; other less common breaks | Only necessary when claiming credits beyond the main form |

How to File a Simple Tax Return

Most people spend 45 minutes to maybe two hours on a simple return if they've got their paperwork organized and nothing weird pops up.

Round up your documents. W-2s from every employer you had during the year arrive by January 31. Any 1099-INT forms reporting interest over $10. Social Security cards for yourself and anyone you're claiming as a dependent. Your bank's routing and account numbers if you want your refund deposited directly (which you do, unless you enjoy waiting extra weeks for a paper check). Kids you're claiming for the Earned Income Tax Credit or Child Tax Credit? You'll need their birth dates and Social Security numbers handy.

Pick how you're filing. Three main paths here: IRS Free File works for anyone earning under $79,000, commercial tax software runs from free to about $60 for basic versions, or the IRS Direct File pilot if you live in one of the 25 participating states. You can still file on paper, but why would you? That adds six to eight weeks to getting your refund.

Fill out the form. Personal info first—your name exactly as it appears on your Social Security card, current address, SSN, and filing status. Pull your wage amount from box 1 of your W-2 and put that on line 1a of the 1040. Got interest income or unemployment? That requires Schedule 1, but most simple filers skip it entirely. Line 12 gets your standard deduction. Software calculates your taxable income automatically. Paper filers subtract manually.

Handle withholding and credits. Box 2 on your W-2 shows federal tax already withheld from your paychecks—that number goes on line 25 of the 1040. Qualify for the Earned Income Tax Credit? Either work through the EIC worksheet or let software figure it. The Child Tax Credit ($2,000 per qualifying child under 17 for 2026) goes on line 19. These credits often turn a tax bill into a refund.

Double-check everything before submitting. Names matching Social Security cards exactly is crucial—even a middle initial difference causes processing delays. If you're setting up direct deposit, triple-check those bank numbers against a voided check or bank statement. E-filing requires electronic signatures through PIN numbers. Paper filing needs physical signatures from both spouses on joint returns. E-filed returns typically process within three weeks, with refunds hitting your account in two to three weeks.

Track what's happening. The IRS "Where's My Refund?" tool goes live 24 hours post-e-filing (or a month after you mail a paper return). You'll enter your Social Security number, filing status, and the exact refund amount from your return. Updates happen once daily, typically overnight.

Author: Benjamin Carte;

Source: atiservicesoftampa.com

Free and Low-Cost Filing Options for Easy Tax Returns

IRS Free File partners with tax software companies to offer completely free federal return prep for anyone earning $79,000 or less—that's roughly 70% of all filers. Critical detail: access these offers through IRS.gov, not the software company's website directly. Go straight to TurboTax or H&R Block's site, and they'll steer you toward paid versions even if you qualify for free.

Each participating company sets additional eligibility rules within that income cap. One might specialize in active military situations, another offers Spanish-language support. Federal filing must be free through these partnerships, though state returns often cost extra. Read the terms before you start—some "free" offers come with aggressive upselling for refund advances or audit insurance.

Volunteer Income Tax Assistance (VITA) provides face-to-face free tax prep for people earning $64,000 or less, anyone with disabilities, and limited English speakers. IRS-certified volunteers run VITA sites at community centers, libraries, and schools from late January through mid-April. Services include e-filing and direct deposit setup. Find locations at IRS.gov or call 800-906-9887.

Tax Counseling for the Elderly (TCE) targets taxpayers 60 and older, with volunteers trained on retirement income quirks and Social Security complications. Many TCE sites operate through AARP Foundation's Tax-Aide program, which despite the name serves all ages. Volunteers get specialized training on issues like required minimum distributions from retirement accounts and how Medicare premiums affect taxes.

The IRS Direct File pilot expanded to 25 states for 2026, letting eligible taxpayers file directly through the IRS website for free using a mobile-friendly interface. It only works for simple situations—W-2 income, standard deduction, common credits. Direct File asks questions in plain English and calculates everything behind the scenes. Current participating states include Arizona, California, Florida, Massachusetts, Nevada, New Hampshire, New York, South Dakota, Tennessee, Texas, Washington, Wyoming, plus 13 states that joined the pilot in late 2025.

Author: Benjamin Carte;

Source: atiservicesoftampa.com

Commercial software free tiers exist, though companies push upgrades constantly. Truly free versions handle W-2 income, standard deduction, Earned Income Tax Credit, and Child Tax Credit without charging a dime. Add unemployment income, interest above $1,500, or HSA contributions, and suddenly the software suggests you "upgrade" for $60.

Common Mistakes That Complicate Simple Returns

Math errors cause more headaches than anything else. Add up two W-2s wrong, transpose numbers when entering your withholding, miscalculate the standard deduction—all preventable. The IRS fixes obvious math mistakes, but correction adds three to six weeks to processing. Software eliminates calculation errors unless you enter the wrong numbers to begin with.

Choosing the wrong filing status messes up your tax calculation and can get you in trouble. Some married couples file as single thinking it saves money—that's tax fraud, not strategy. Head of household requires specific qualifications: you paid more than half the household expenses and had a qualifying person living with you over half the year. Claiming it without meeting those tests invites IRS scrutiny.

Forgetting to sign your return sounds trivial but makes it invalid. E-filed returns need electronic signatures through PIN numbers. Paper returns require actual signatures from both spouses on joint filings. Unsigned returns sit unprocessed while the IRS requests signatures, delaying your refund for months.

Bank account mistakes kill direct deposit. Transposed routing numbers, accounts you closed last year, accidentally entering someone else's account—all these force the IRS to mail paper checks instead. Check those numbers three times against a voided check or online banking.

Missing or mismatched forms create serious problems. Forgot to attach a W-2 with your paper return? Failed to report all W-2s when e-filing? The IRS gets copies directly from your employer and matches them against your return. Mismatches generate automated letters and can trigger audits. If you get a corrected W-2 after filing, you'll need to file an amended return on Form 1040-X.

Social Security number mismatches between your tax return and Social Security Administration records cause immediate e-file rejections. This happens constantly when people change their name through marriage or divorce but forget to update their Social Security card. Your return name must match SSA records exactly—same spelling, same hyphens, same suffixes.

Author: Benjamin Carte;

Source: atiservicesoftampa.com

When Your Tax Situation Is No Longer Simple

Earning $400 or more from self-employment changes everything. Now you need Schedule C for business profit and loss plus Schedule SE for self-employment tax. Driving for DoorDash twice a month, writing freelance articles, selling crafts on Etsy—all these trigger those requirements. You'll track business expenses, potentially calculate quarterly estimated payments, and maybe deal with home office complications. Most people at this point benefit from professional help or premium software.

Investment income beyond basic savings account interest gets messy fast. Sold some stock? You'll need Form 8949 and Schedule D to report capital gains and losses, plus you need to know your cost basis. Dividend income over $1,500 requires Schedule B. Cryptocurrency transactions, which the IRS now watches closely, demand detailed reporting of every sale, trade, or conversion. Selling stock you bought all at once might seem straightforward, but if you accumulated shares over time, you're calculating separate gains for each purchase.

Rental property income requires Schedule E and potentially Form 4562 for depreciation. Even renting out your spare bedroom creates reporting obligations. You'll deduct expenses proportionally, distinguish between improvements and repairs, and navigate passive activity loss limitations. Airbnb or VRBO income adds complications around personal use days versus rental days.

Itemizing deductions makes sense when your total exceeds the standard deduction, but demands Schedule A and serious documentation. Medical expenses only help when they exceed 7.5% of your adjusted gross income—a high bar. Charitable donations need receipts, and anything over $250 requires written acknowledgment from the charity. State and local taxes max out at $10,000 deductible, limiting benefits for high-tax-state residents.

Education credits beyond straightforward scenarios require Form 8863 and detailed expense tracking. The American Opportunity Tax Credit and Lifetime Learning Credit phase out at higher incomes, define "qualified expenses" narrowly, and have coordination rules that complicate otherwise simple filings. Even the student loan interest deduction, though relatively simple, still needs Form 1098-E and navigates income limitations.

The biggest mistake I see is taxpayers assuming complexity where none exists, paying for professional help they don't need.Conversely, some people insist on DIY filing when their situation clearly requires expertise—like when they start a business mid-year but don't realize they owe quarterly taxes. Recognizing which category you fall into saves money and prevents costly errors

— Jennifer Martinez

Health Savings Accounts require Form 8889 even though they're designed to be tax-advantaged. You'll report what your employer contributed, what you contributed, and any distributions, making sure you stay under contribution limits ($4,300 individual, $8,550 family for 2026) and use money only for qualified medical expenses.

Foreign income or accounts trigger FBAR reporting (FinCEN Form 114) and potentially Form 8938 when foreign assets exceed certain thresholds. Even a modest bank account overseas that you inherited creates reporting requirements with harsh penalties for non-compliance.

Frequently Asked Questions About Simple Tax Returns

Filing a simple tax return in 2026 stays accessible and often completely free for most American wage earners. What determines your path isn't income amount—it's income source and whether you're itemizing deductions.

Honest self-assessment matters here. One or two W-2s, the standard deduction, and common credits like the Child Tax Credit or Earned Income Tax Credit? You're simple. Add self-employment income, investment sales, rental property, or itemized deductions, and you've crossed into complexity requiring different tools and possibly professional guidance.

Free resources exist specifically for basic filings. IRS Free File, VITA sites, and the expanding Direct File program eliminate cost barriers while delivering accuracy through guided questions and automatic calculations. These aren't inferior options—they're purpose-built for straightforward returns and often work better than paid alternatives for simple situations.

Watch for triggers moving you from simple to complex. That first freelance client, inherited stock from a relative, or deciding to rent your basement changes filing requirements. Recognizing these transitions early lets you prepare properly instead of discovering complications on April 14.

File on time even when you can't pay immediately. The failure-to-file penalty (5% monthly, maxing at 25% of unpaid tax) crushes the failure-to-pay penalty (0.5% monthly). Simple returns take minimal time to complete, making late filing inexcusable for most taxpayers. Set up direct deposit, file electronically, and track your refund through official IRS tools rather than relying on software company timelines.

Your tax situation evolves. What's simple today might grow complex as you launch a business, invest in real estate, or manage retirement distributions. Building basic tax literacy now—understanding what keeps a return simple and recognizing when you've crossed that threshold—prepares you for whatever financial changes come next.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to tax filing, tax software, IRS forms, deadlines, and general tax preparation processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Tax filing requirements may vary depending on individual circumstances, income sources, residency status, and applicable laws.

This website does not provide tax, legal, or financial advice, and the information presented should not be used as a substitute for consultation with a qualified tax professional or advisor.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.