Business owner preparing S corporation tax return online on laptop

How to File S Corp Online

Most S corporation owners discover the tax filing process feels different than what they expected. You've set up your business structure to avoid the double taxation trap that catches C corporations, but now you're dealing with pass-through taxation mechanics that create their own paperwork demands.

Electronic filing has become the standard approach—not because the IRS mandates it for every business (though they're heading that direction), but because paper filing now feels like sending a telegram when everyone else uses email. The infrastructure, the processing times, even the way tax professionals work—everything points toward digital submission.

If you're running an S corp, you'll file whether you had a profitable year or not. The return documents what happened financially, allocates income and losses to shareholders, and creates the K-1 schedules that shareholders need for their personal returns. Getting this done correctly and on time matters more than most people realize until they face late-filing penalties.

What Is S Corporation Tax Filing

Every S corporation files Form 1120-S each year. This document shows the IRS your business's financial activity: what you earned, what you spent, which deductions you're claiming, and any credits you qualify for.

The form doesn't actually calculate a tax bill for the corporation itself. Instead, Form 1120-S allocates everything to shareholders based on ownership percentages. Each shareholder gets a Schedule K-1 that breaks down their share of corporate income, deductions, and credits. They take these numbers to their personal tax returns (Form 1040), where the actual tax gets calculated and paid.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Think of it this way: your S corp return tells a story about the business year, then divides that story into chapters for each owner. The owners pay tax on their chapters when they file individually.

There are exceptions—S corporations sometimes owe tax on built-in gains if they converted from C corporation status, or on excess passive income if they hold too many investments while having C corp earnings and profits. But for most S corporations, the entity itself doesn't write a check to the IRS.

Why go electronic? The IRS systems check your return immediately when you submit it. Math errors get caught before acceptance, not months later. Missing schedules trigger alerts during submission, not rejection letters in June. You receive confirmation within 48 hours typically, compared to wondering for weeks whether your mailed return arrived safely.

Filing electronically also builds your digital records automatically. Your software keeps copies of everything submitted. Need to reference last year's depreciation schedule or compare shareholder distributions? You're searching a file, not a filing cabinet.

IRS Requirements for Electronic S Corp Filing

The IRS requires electronic filing from tax preparers who handle 10 or more returns annually. This catches nearly every CPA, enrolled agent, and tax firm. If you hire a professional, your return will go through e-file channels whether you prefer it or not.

For businesses preparing their own returns, e-filing is encouraged but not legally mandatory—yet. The agency has clearly indicated they want to phase out paper processing. Their systems are designed for digital files, and the resources devoted to paper processing shrink each year.

You'll need your business's Employer Identification Number before you can file. This nine-digit identifier works like a Social Security number for your corporation. You also need accurate information for every shareholder: full legal names, Social Security numbers (or ITINs for non-resident aliens), and current addresses.

The IRS doesn't let you just email a PDF. Electronic filing works through authorized providers—software companies and tax professionals enrolled in the e-file program who meet IRS security standards and use approved transmission formats.

For calendar-year S corporations (most of them), the filing deadline lands on March 15. Fiscal-year corporations file by the 15th day of month three after their year-end. A corporation with a June 30 fiscal year-end files by September 15.

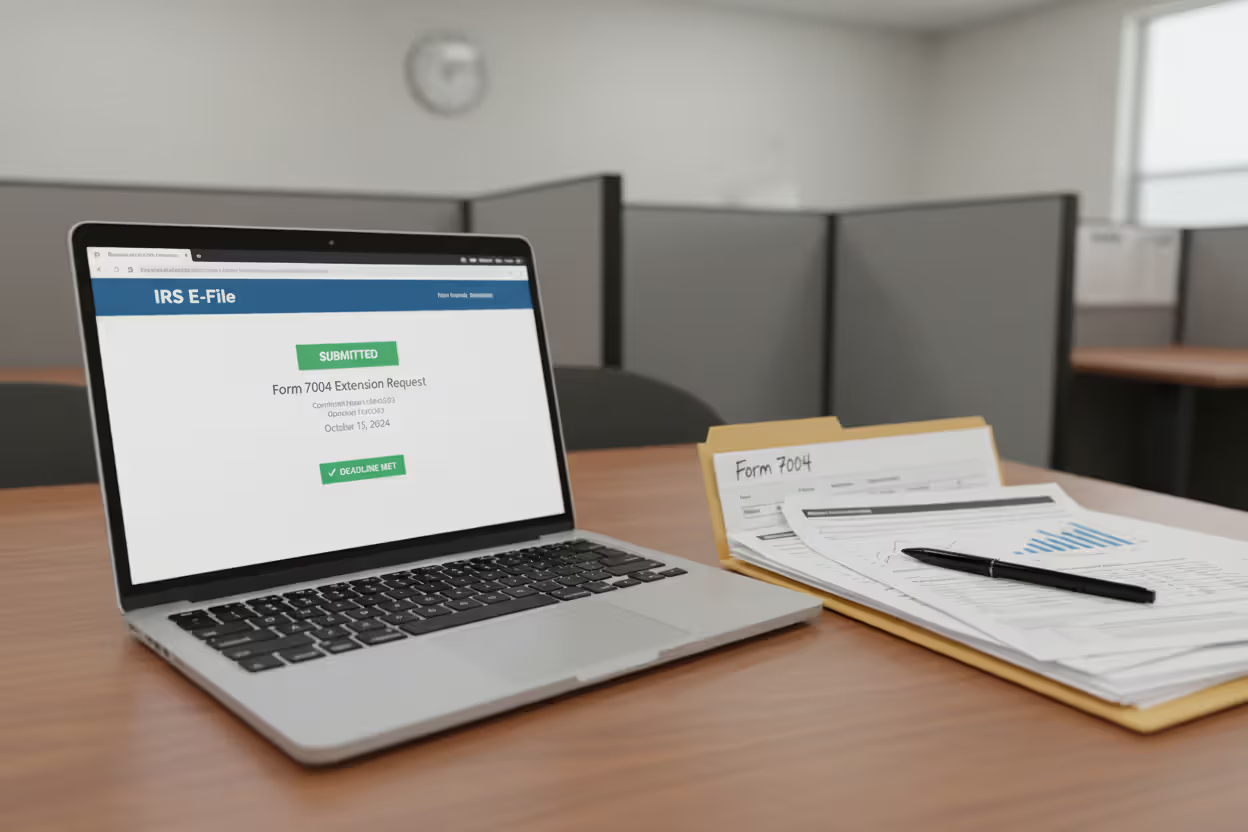

Need more time? File Form 7004 before the original deadline to get an automatic six-month extension. This moves calendar-year filers to September 15. But here's the catch: extensions give you more time to file, not more time to pay any tax owed. Interest starts accumulating on unpaid balances from the original deadline regardless of extensions.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Electronic filing systems accept returns around the clock during filing season, though weekend submissions process on the following Monday. The IRS typically opens business e-file systems in mid-January.

Step-by-Step Process to File S Corporation Taxes Online

Gathering Required Documents and Information

Start with your complete financial picture. Pull profit and loss statements, balance sheets for year-end and year-start, depreciation schedules, and detailed records of every income source and expense category.

If you use accounting software like QuickBooks, Xero, or FreshBooks, generate these reports directly from your system. The data's already there—you're just formatting it for tax purposes.

Compile everything related to your shareholders. Ownership percentages matter enormously because they determine income allocation. Document any ownership changes during the year—shareholders who bought in or sold out mid-year need prorated K-1s. Calculate or update stock basis for each shareholder, tracking contributions, distributions, income, and losses that affect basis.

Gather documentation for any credits you're claiming. Did you invest in research and development? Claim energy efficiency improvements? Hire workers from targeted groups? Each credit needs supporting records before you start entering numbers into tax forms.

Check last year's return carefully. Your balance sheet on line one of this year's Schedule L must match the final balance sheet from last year's return, line by line. Carryforward items—net operating losses, charitable contributions beyond the annual limit, credit carryforwards—need precise tracking from prior years.

Choosing an E-File Method

You've got three main paths: buy commercial software and do it yourself, hire a tax professional to handle everything, or use a hybrid approach where you enter data and a professional reviews it.

Commercial software like TurboTax Business, TaxAct Business, or H&R Block Premium & Business works through interview questions. The software asks about your income sources, expenses, shareholders, and deductions, then fills in the appropriate forms based on your answers. These platforms work well if your S corp has straightforward operations—one state, a few shareholders, regular business income without complex investments or international activities.

Tax professionals (CPAs, enrolled agents, tax attorneys) bring expertise to complicated situations. They handle the entire filing process, but more importantly, they apply strategic knowledge about deductions you might miss, allocation issues you didn't know existed, and potential problems worth avoiding. Professional preparation costs more but can save you multiples of the fee by preventing mistakes.

Some accounting firms offer a middle option: you use their client portal to enter financial data, and they review, correct if needed, and submit your return. You pay less than full-service preparation but still get professional oversight.

Submitting Your Return Electronically

Once you've entered all information, your software or preparer generates the complete return—Form 1120-S, all required schedules, and a K-1 for each shareholder.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Review everything methodically. Check shareholder names character-by-character against Social Security cards. Verify Social Security numbers. Confirm ownership percentages add up to exactly 100%. Compare Schedule K-1 totals against the amounts shown on the corporate Schedule K—they must match exactly.

You'll electronically sign the return using one of two methods. The Self-Select PIN approach lets corporate officers create a five-digit PIN that serves as their signature. Alternatively, Form 8879-S authorizes your e-file provider to attach your signature to the return electronically. Every officer who must sign needs to provide authorization.

After submission, you receive an acknowledgment within 24 to 48 hours. This acknowledgment number proves the IRS accepted your return. Save it permanently with your tax records.

If the IRS rejects your return, you'll get an explanation. Common rejection reasons: names don't match Social Security records exactly, the EIN was already used to file a return for this year, Social Security numbers are incorrect or belong to deceased individuals, or required forms are missing.

The IRS doesn't mail confirmation letters for accepted e-filed returns. Your electronic acknowledgment is your proof of filing. Save your complete return, all schedules, K-1s, and the acceptance confirmation for at least seven years—longer if you have property with basis tracking or carryforward items.

S Corp Filing Software Options and Comparison

Choosing software depends on your business complexity, how many states you file in, and your comfort level navigating tax concepts. Here's what major platforms offer:

| Software Name | Price Range | Key Features | Best For | IRS-Authorized |

| TurboTax Business | $180-$230 | Question-based navigation, unlimited support via phone, each state return costs extra ($50) | S corps with simple operations, owners new to business tax filing | Yes |

| TaxAct Business | $120-$165 | Lower pricing tier, solid customer support, federal e-file included at no extra charge | Budget-conscious businesses with straightforward returns | Yes |

| H&R Block Premium & Business | $125-$180 | Option to visit local offices for help, handles multi-state situations well | Businesses that value access to in-person assistance | Yes |

| Drake Tax | $350-$495 (professional tier) | File unlimited returns on one license, advanced features, built for tax preparers | High-volume filers, tax professionals managing multiple clients | Yes |

| ProConnect Tax Online | $500+ annually | Cloud-based access, integrates directly with QuickBooks, detailed reporting tools | Growing S corps with sophisticated accounting needs | Yes |

| FreeTaxUSA Business | $120-$150 | Budget-friendly option, clean interface without excessive guidance | Very simple S corps with minimal transactions | Yes |

These prices reflect current federal return costs. State returns typically add $40 to $60 per state. Some platforms bundle multiple state returns or include prior-year amendments in their pricing.

Professional-grade software like Drake Tax or ProConnect doesn't walk you through interview questions—you need to understand which forms and schedules apply to your situation. These platforms provide flexibility for complex scenarios but assume tax knowledge.

Consumer-focused software like TurboTax Business provides extensive guidance but sometimes struggles with unusual situations. If your S corp has foreign shareholders, significant passive investment income, or built-in gains from a C corporation conversion, you'll want either professional software or a tax preparer who handles these issues regularly.

Common Mistakes When Filing S Corp Returns Electronically

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Shareholder information errors top the rejection list. The IRS cross-checks every name and Social Security number against Social Security Administration databases. When a shareholder recently married and changed their name but you use the new name with the old Social Security number, the system rejects the return. Always verify current legal names match Social Security records before submission.

Missing Schedule K-1 forms create immediate problems. You need a K-1 for every shareholder, and the K-1 totals must match the corporate Schedule K exactly. Software catches these discrepancies usually, but manual data entry creates opportunities for typos and transposition errors.

Basis calculations confuse many S corp owners. Shareholders can only deduct losses up to their stock basis plus any loan basis. The K-1 allocates losses, but tracking basis is the shareholder's responsibility. You can file a return allocating losses to shareholders with insufficient basis—the IRS won't reject it immediately—but it creates problems later when examining individual returns.

Deadline confusion happens when businesses mix up calendar-year and fiscal-year requirements. A fiscal-year S corporation with a June 30 year-end files by September 15, not March 15. Electronic systems won't stop you from filing at the wrong time—they accept returns whenever submitted.

Signature authorization issues delay returns frequently. S corporations require an officer signature—president, vice president, treasurer, or assistant treasurer typically. The person signing must have authority under your corporate bylaws. Using an unauthorized person's PIN raises questions and can trigger rejection.

The biggest mistake I see with S corporation e-filing is rushing through the process in the final week before the deadlineюShareholders need their K-1s to file personal returns, so any error in the S corp return cascades into problems for multiple people. Taking time to review shareholder basis, distributions, and income allocations prevents most issues we encounter

— Michael Chen

Forgetting state returns leaves compliance gaps. Filing federally doesn't satisfy state obligations. Most states require separate S corporation returns. Some states don't even recognize S election, treating your entity as a C corporation for state tax purposes. Check requirements for every state where you do business, have employees, own property, or have created nexus through sales activity.

Costs and Fees for Electronic S Corp Filing

The IRS charges nothing to file Form 1120-S electronically. Unlike certain states that impose e-file fees, federal electronic filing is free at the agency level.

Software costs range from roughly $120 to $500 for federal returns, as detailed in the comparison table. Each state return adds $40 to $60 typically. Filing in five states might cost you $300 to $400 just for state returns beyond the federal software.

Professional preparation fees vary dramatically based on complexity, credentials, and location. Simple S corporation returns prepared by a CPA or enrolled agent typically run $800 to $1,500. Complex returns involving multiple shareholders, numerous states, or unusual transactions can cost $2,500 to $5,000 or more.

Author: Lauren Whitma;

Source: atiservicesoftampa.com

Fee structures vary by preparer. Flat fees work for straightforward situations. Hourly billing makes sense for complex work where the time investment is uncertain. Hourly rates for qualified tax professionals range from $150 to $400 per hour depending on credentials, experience, and geographic location. Urban markets see higher rates than rural areas.

Bookkeeping adds cost if your records aren't organized. Many tax professionals require clean books before they'll prepare returns—they're preparers, not bookkeepers. Monthly bookkeeping services cost $200 to $1,000 depending on transaction volume, though this expense benefits your entire business operation, not just tax season.

Extension filing (Form 7004) carries no IRS fee whether filed electronically or on paper. Remember though, extensions don't extend time to pay taxes owed. The IRS assesses interest and potentially penalties on late payments even when you've properly extended your filing deadline.

Amended returns filed electronically may cost extra depending on your software. Some licenses include amendments; others charge separately for Form 1120-S amendments. Check your software terms before assuming amendments are included.

Frequently Asked Questions About S Corp Online Filing

Can I file my S corp tax return online myself?

Yes, you can absolutely file without hiring a professional. Commercial tax software walks you through the process with structured questions. But S corp returns are genuinely more complex than individual returns—you're dealing with shareholder basis, distribution rules, income allocation methods, and balance sheet preparation. Simple S corporations (one or two shareholders, straightforward income, single state) work fine for self-filing. Multiple shareholders, complex transactions, or multi-state operations really benefit from professional help. Consider your own tax knowledge honestly before deciding.

What is the deadline for filing S corporation taxes electronically?

Calendar-year S corporations face a March 15 deadline. Fiscal-year S corporations must file by the 15th day of the third month after their tax year closes. When the deadline lands on Saturday, Sunday, or a federal holiday, it shifts to the next business day. You can get an automatic six-month extension by filing Form 7004 before the original deadline—this pushes calendar-year corporations to September 15. But extensions only extend filing time, not payment time. Any tax owed accrues interest from the original deadline forward.

Does the IRS require S corporations to file electronically?

The IRS mandates electronic filing from tax preparers handling 10 or more returns annually. If you hire a CPA, enrolled agent, or tax prep firm, they must file electronically by law. S corporations preparing their own returns aren't legally required to e-file currently, though the IRS strongly pushes in that direction. Paper filing means longer processing times, higher error rates, and weeks of uncertainty about whether your return was received. Most tax software now includes e-filing as a standard feature, making electronic submission the default practical choice even without a legal mandate.

How much does s corp filing software typically cost?

Consumer-focused federal S corporation software costs between $120 and $230—platforms like TurboTax Business or TaxAct Business fall in this range. Professional-grade software runs $350 to $500 or more annually. Each state return adds $40 to $60. These prices cover one federal return and electronic submission. Some platforms charge extra for phone support, amendments, or access to prior-year returns. Professional preparation by a CPA or enrolled agent costs $800 to $1,500 for straightforward returns—significantly more for complex situations involving multiple states or unusual transactions.

What happens if I miss the S corp filing deadline?

Missing the March 15 deadline without filing an extension triggers late-filing penalties immediately. The IRS charges $210 per month (or partial month) per shareholder, up to 12 months maximum. An S corp with three shareholders filing two months late faces $1,260 in penalties ($210 × 2 months × 3 shareholders). These penalties apply even when the corporation owes zero tax. Filing Form 7004 before the original deadline prevents late-filing penalties if you submit the actual return by the extended deadline. Reasonable cause exceptions exist but require written explanation and supporting documentation—"I forgot" doesn't qualify.

Do I need a special ID to file my S corp return online?

You need your Employer Identification Number (EIN)—the nine-digit number identifying your business to the IRS. You also need Social Security numbers or ITINs for all shareholders. To electronically sign the return, corporate officers create a Self-Select PIN—a five-digit number you choose during the filing process. Alternatively, you can authorize your e-file provider to sign on your behalf using Form 8879-S. No special IRS account or separate registration is required beyond using approved e-file software or a professional enrolled in the IRS e-file program.

Conclusion

Electronic filing has transformed S corporation tax compliance from a paper-heavy annual headache into a streamlined digital process. Real-time validation catches errors immediately. Processing happens faster. Record-keeping becomes automatic. E-filing simply works better than paper for virtually every S corporation.

Success comes from preparation. Organized financial records, accurate shareholder data, and a solid understanding of your business's tax situation create the foundation for smooth filing. Match your software or professional help to your actual complexity level and budget reality.

The March 15 deadline arrives fast after year-end closes. Starting your tax prep in January or early February gives you time to gather documents, resolve questions, and file without deadline panic. Remember that shareholders need timely K-1s to complete their personal returns—your S corp filing isn't just about the business, it's a critical step in everyone's tax process.

Whether you handle filing yourself through software or work with a tax professional, electronic submission delivers confirmation, accuracy, and efficiency that paper filing simply cannot match. The modest investment in proper filing tools and adequate preparation time prevents expensive penalties and creates confidence that your S corporation met its federal obligations correctly and completely.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to tax filing, tax software, IRS forms, deadlines, and general tax preparation processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Tax filing requirements may vary depending on individual circumstances, income sources, residency status, and applicable laws.

This website does not provide tax, legal, or financial advice, and the information presented should not be used as a substitute for consultation with a qualified tax professional or advisor.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.