Person reviewing tax documents at a desk before filing a tax extension

What Is a Tax Extension and How Does It Work

Content

Content

Can't get your tax return done by mid-April? You're not alone—millions of Americans file for a tax extension every year. This straightforward IRS process pushes your filing deadline from spring all the way to mid-October, giving you six extra months to get your paperwork together.

Here's the catch that trips people up: getting more time to file doesn't mean you get more time to pay. That's a huge distinction. If you owe the IRS money, that bill is still due in April, extension or not. Skip that payment, and you'll rack up penalties and interest through October—even if you filed your extension perfectly.

Why would you want an extension in the first place? Maybe you're still waiting on a corrected 1099 from your brokerage. Perhaps you sold rental property and need time to calculate depreciation recapture. Or maybe you just started a side business and your bookkeeping is a mess. Whatever the reason, the IRS doesn't care. They'll grant you the extra time without asking questions.

The bottom line: an extension buys you time to file accurately, not time to pay what you owe. Get that distinction right, and you'll avoid costly mistakes.

When You Can Request a Tax Filing Extension

Good news first: the IRS makes extension requests remarkably easy. You don't need to justify why you need one. No proof required. No explanation necessary. Just file the paperwork by April 15, and you've automatically got until October 15.

Anyone can request an extension—high earners, low earners, single filers, married couples, self-employed individuals, retirees. Your tax situation's complexity doesn't matter. Whether you've got one W-2 or twenty K-1s from various partnerships, the process stays the same.

You'll use IRS Form 4868. That's the official form titled "Application for Automatic Extension of Time To File U.S. Individual Income Tax Return." The word "automatic" isn't marketing fluff—if you submit it on time, you get the extension. No waiting for approval letters. No wondering if you qualify.

Some taxpayers get extensions without filing anything at all. Living abroad on tax day? You automatically get until June 15 if you're a U.S. citizen or resident alien. Military personnel serving in combat zones get their deadline extended by at least 180 days after they leave the combat area. When hurricanes, wildfires, or other disasters strike, the IRS often announces automatic extensions for affected regions.

But here's what trips people up every single year: getting extra time to file your return doesn't extend your payment deadline one single day. Owe $5,000? That money needs to reach the IRS by mid-April. Pay less than 90% of what you actually owe, and penalties start piling up immediately—extension or no extension.

Author: Derek Langston;

Source: atiservicesoftampa.com

How to File for a Tax Extension

Filing for an extension takes less time than standing in line at the post office. You've got two routes: electronic filing or paper Form 4868. Both cost nothing. Both work fine. Electronic just works faster and gives you instant proof.

If your adjusted gross income falls below $79,000 (for 2026 taxes), you can use IRS Free File—totally free software that includes extension filing. Make more than that? TurboTax, H&R Block, and other commercial programs handle extensions as part of their basic service. Your CPA or tax preparer can file one electronically for you, too.

The electronic form wants basic information: your name, address, Social Security number, and your best guess at your total tax bill for the year. Planning to send money with your extension? You'll enter that amount and choose how to pay. Start to finish, expect to spend maybe 15 minutes max.

There's actually a shortcut that's even faster: if you're paying taxes anyway, just make a payment through IRS Direct Pay or EFTPS (the Electronic Federal Tax Payment System) by April 15 and mark it as an extension payment. The IRS counts the payment itself as your extension request. No separate form needed. This only works if you're paying enough to cover most or all of what you owe.

Want to go old-school with paper? Download Form 4868, fill it out, and mail it to the address listed in the instructions (the address changes based on where you live). Just make absolutely sure it's postmarked before April 15. Unlike electronic filing, you won't know if it arrived safely unless you pay for tracking.

Filing Electronically vs. Mailing Form 4868

Electronic filing beats paper filing in almost every way. You get confirmation within seconds that your extension went through. That confirmation email or receipt becomes your proof if questions come up later. The software catches mistakes before you submit—missing Social Security numbers, math errors, formatting problems.

Paper filing? You're flying blind. The IRS takes weeks to process paper forms, sometimes over a month during the April rush. Mail gets lost. Forms get separated from envelopes. Without delivery confirmation, you can't prove you mailed anything. If your Form 4868 never shows up in IRS systems, you don't have an extension, regardless of when you dropped it in the mailbox.

The timeline difference is dramatic. E-file your extension and you'll see acknowledgment within minutes. Full processing wraps up in a day or two. Mail a paper form and you might wait six weeks to see it appear in your IRS account—assuming it appears at all. Your postmark date determines whether you're on time, but that doesn't help much if the form vanishes somewhere between your mailbox and Kansas City.

Cost-wise, they're identical if you use Free File for electronic submission. Through commercial software, you might pay $30-40, which is roughly what you'd spend on tracking and certified mail anyway. Unless you genuinely lack internet access or have unusual circumstances, electronic filing makes more sense for just about everyone.

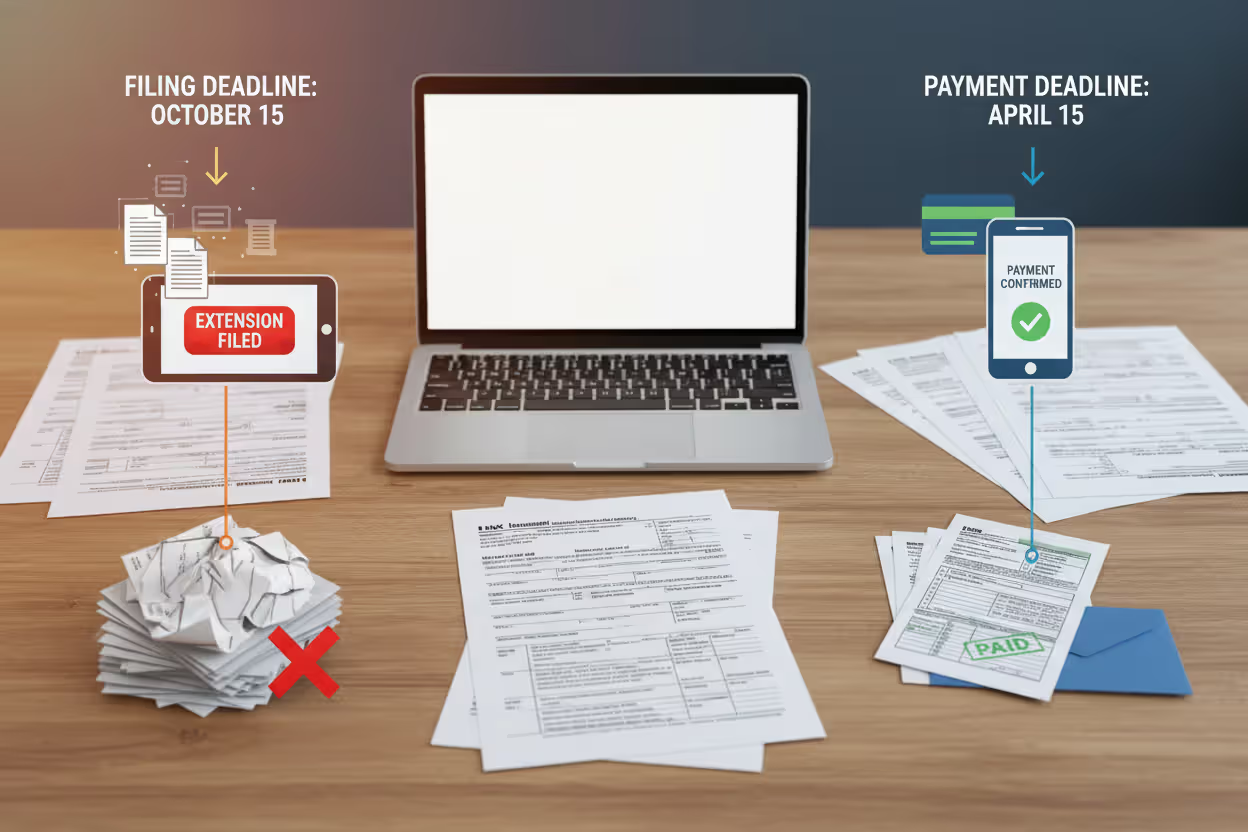

What a Tax Extension Does and Does Not Cover

Let's be crystal clear: an extension gives you six more months to file your paperwork. That's it. That's all it does. The confusion around this costs taxpayers serious money every year.

What you do get: until mid-October to finish and submit your federal return without facing late-filing penalties. You can take time to track down missing documents, work through complicated investment sales, meet with your accountant multiple times, or just deal with whatever life threw at you in April. The extension also keeps your IRA contribution window open longer, since you can contribute for the previous tax year up to your filing deadline, including extensions.

What you don't get: more time to pay your tax bill. If you owe money, that's due April 15. Period. Interest starts accruing April 16 on any unpaid balance. So do penalties. The extension doesn't freeze your payment obligations or put them on hold.

This confusion creates real financial pain. Taxpayers file extensions, assume they're all set, then don't think about taxes again until September or October. When they finally file and pay, they're shocked to discover they've accumulated six months of penalties and interest. On a $5,000 tax bill, those extra costs can hit $200 or more.

The biggest mistake I see with extensions? People think they're postponing their payment deadline.They're not. File an extension when you owe $10,000, then pay nothing until October, and you've just donated several hundred dollars in penalties and interest that you didn't need to pay

— Jennifer Martinez

Some taxpayers worry that requesting an extension raises red flags at the IRS or increases audit risk. Neither is true. Extensions are routine—completely normal and incredibly common. The IRS doesn't flag your return as suspicious just because you needed extra time. Your audit odds depend on what's in your return, not when you filed it.

Extensions don't affect refunds either, except that you wait longer to get your money back. The IRS doesn't pay you interest on refunds when you've filed under extension, so you're basically giving the government a free loan for six extra months.

Author: Derek Langston;

Source: atiservicesoftampa.com

Tax Extension Deadlines and Key Dates

April 15 is tax day for most Americans filing individual returns. When April 15 falls on a weekend or federal holiday, the deadline moves to the next business day. For 2026, April 15 is a Wednesday, so that's your deadline for both filing and paying.

File Form 4868 by April 15, and your new filing deadline becomes October 15, 2026. This six-month extension happens automatically—no approval process, no waiting period. October 15 is a Thursday in 2026, so no adjustment there either.

State deadlines get messier. Many states automatically honor your federal extension—file federal Form 4868, and your state return gets extended too without any extra paperwork. But plenty of states do their own thing. Some need separate forms. Others extend everyone automatically without requiring any forms at all.

Take California—they give everyone an automatic six-month extension without any forms, though you'd better pay at least 90% of what you owe by the original deadline. New York wants you to file Form IT-370 for a state extension, even if you've already filed federally. Virginia usually accepts your federal extension automatically, but you should verify that each year since rules change.

Critical dates you need to lock in: April 15 is your deadline for both requesting the extension and paying estimated taxes. October 15 is your extended filing deadline. Miss the April deadline to request an extension, and you need to file your complete return by April 15 or face late-filing penalties. Miss the October extended deadline, and penalties calculate based on how many months late you filed.

If you pay estimated quarterly taxes, those deadlines run on their own schedule regardless of extensions. April 15, June 15, September 15, and January 15—those quarterly payment dates don't change just because you extended your annual return filing.

Author: Derek Langston;

Source: atiservicesoftampa.com

Penalties and Interest When You Extend Filing

Filing an extension eliminates late-filing penalties, but it doesn't stop penalties and interest from growing on unpaid taxes. Understanding what these charges cost helps you make smarter decisions about when and how much to pay.

The failure-to-pay penalty runs 0.5% of your unpaid taxes each month, capping at 25% total. Owe $8,000 and pay nothing from April through October? That's roughly $240 in penalties alone (six months × 0.5% × $8,000). This penalty applies to your net tax due after withholding and credits, not your total tax liability.

Interest piles on top of that. The IRS sets interest rates quarterly based on the federal short-term rate plus 3%. For 2026, individual rates hover around 7-8% annually. Interest compounds daily, meaning you pay interest on your interest. That same $8,000 balance from April to October generates about $280-320 in interest depending on exact rates.

Add it up: penalties and interest on $8,000 in unpaid taxes from April to October could total $520-560. That's money you could save by either paying on time or at least paying as much as possible in April and settling up later.

The penalty structure rewards paying at least 90% of your total tax bill by April. Hit that 90% threshold, and you'll significantly reduce or even eliminate the failure-to-pay penalty, though interest keeps running on whatever's left unpaid. Pay 100% by April, and you owe nothing extra regardless of when you file your return (within the extension period).

Partial payments make a real difference. You owe $6,000 but can only scrape together $4,000 by April? Pay that $4,000. Now penalties and interest only calculate on the remaining $2,000, not the full $6,000. Every dollar you pay by the original deadline saves you money on penalties and interest.

The IRS can waive penalties under reasonable cause—serious illness, natural disasters, inability to access records because of circumstances beyond your control. But they never waive interest. Ever. If you've got legitimate reasons for late payment, you can request penalty abatement after filing, though the interest bill stands.

Common Mistakes to Avoid When Filing an Extension

Author: Derek Langston;

Source: atiservicesoftampa.com

The single costliest mistake? Filing for an extension without sending estimated tax payments. If you owe money, you must pay by April, even if you're not filing your return until October. Thinking the extension covers both filing and payment leads to penalties that can easily reach hundreds or thousands of dollars on bigger tax bills.

Underestimating your tax liability comes in as a close second. Form 4868 asks you to estimate your total tax for the year, then subtract what you've already paid through withholding and estimated payments. Plenty of people lowball this estimate to reduce their April payment. Bad strategy. Estimate too low and pay too little by April, and you'll face penalties on the shortfall.

Better approach: pull up last year's return and use that as your starting point, adjusting for things you know changed. Got a raise? Estimate higher. Took a big deduction last year that won't repeat? Estimate lower. Tax software can generate quick estimates if you've got most of your documents ready.

Ignoring state extensions causes double trouble. Your federal extension doesn't automatically handle state requirements everywhere. Some states need separate forms. Others have different payment rules. Miss your state extension requirements, and you could face state penalties even though your federal extension was perfect.

Check your state tax agency's website or ask your tax professional about state-specific extension rules. States that need their own forms usually keep the same April deadline as the federal extension.

Missing the extension deadline entirely happens more than you'd think. Some people plan to file extensions, then get busy and suddenly it's April 16. Once April 15 passes without either a complete return or an extension form, you're facing late-filing penalties. The failure-to-file penalty is brutal—5% per month up to 25%, ten times worse than the failure-to-pay penalty.

Realize on April 16 that you missed both deadlines? File your return immediately. Don't wait. Late-filing penalties calculate by the month, so late April filing costs dramatically less than waiting until May or later.

Not keeping extension records bites taxpayers during audits or IRS inquiries. Save your Form 4868 confirmation—the electronic receipt or your certified mail tracking for paper forms. If the IRS later claims you filed late, this confirmation proves you requested the extension on time.

Finally, some people file extensions every single year without addressing why they need them. If you're constantly scrambling to meet deadlines because of disorganization or an overwhelming tax situation, that's a sign you need to change your approach. Consider hiring a tax professional, improving your record-keeping throughout the year, or adjusting your withholding to avoid big tax bills that create April stress.

Tax Extension vs. No Extension: Deadlines, Penalties, and Requirements

| Your situation | When your return is due | When payment is due | Penalty for late filing | Penalty for late payment | Do you need to file a form? |

| You don't request extra time | April 15, 2026 | April 15, 2026 | 5% each month (up to 25%) if you file late | 0.5% each month (up to 25%) if you pay late | No |

| You get an extension and pay your full tax bill by April | October 15, 2026 | April 15, 2026 | None if filed by Oct 15 | None | Yes (Form 4868) |

| You get an extension and pay 90% or more by April | October 15, 2026 | April 15, 2026 | None if filed by Oct 15 | Smaller penalty on remaining balance | Yes (Form 4868) |

| You get an extension but pay nothing by April | October 15, 2026 | April 15, 2026 | None if filed by Oct 15 | 0.5% each month on unpaid balance | Yes (Form 4868) |

| You get an extension but never file by October | N/A | April 15, 2026 | 5% each month starting from April 15 | 0.5% each month starting from April 15 | You submitted Form 4868 but abandoned the return |

Frequently Asked Questions

A tax extension gives you breathing room when you need more time to prepare an accurate return. The request process is simple, free, and requires just basic information submitted by April. But remember: the extension only applies to filing your paperwork, not paying your tax bill.

The smartest approach? Estimate what you owe and pay it by April 15, even if you're not filing your return until October. This strategy eliminates failure-to-pay penalties and keeps interest charges minimal. Can't pay the full amount? Pay whatever you can—each dollar paid by April saves you money on penalties and interest.

Don't fall into the common trap of treating an extension as a payment postponement. Calculate your liability, send payment by April 15, and use the extra time to prepare a thorough, accurate return. Whether you're waiting for corrected tax forms, dealing with complicated investment sales, or just need more time to organize records, an extension provides that time without penalties—as long as you handle the payment piece correctly.

Remember that state requirements vary from federal rules, so check your state's extension process separately. Save confirmation of your extension filing, watch that October deadline, and get your completed return in before time runs out. Used correctly, a tax extension reduces stress and helps you file a more accurate return instead of rushing through one in April.

Related Stories

Read more

Read more

The content on this website is provided for general informational and educational purposes only. It is intended to explain concepts related to tax filing, tax software, IRS forms, deadlines, and general tax preparation processes.

All information on this website, including articles, guides, and examples, is presented for general educational purposes. Tax filing requirements may vary depending on individual circumstances, income sources, residency status, and applicable laws.

This website does not provide tax, legal, or financial advice, and the information presented should not be used as a substitute for consultation with a qualified tax professional or advisor.

The website and its authors are not responsible for any errors or omissions, or for any outcomes resulting from decisions made based on the information provided on this website.